IMF downgrades Pakistan’s GDP growth rate to 2%

GDP growth rate would rebound in the next fiscal 2023-24 up to 4.4%, says IMF

February 01, 2023

- IMF paints bleak picture of Pakistan's economy.

- IMF lifts 2023 growth forecast on China reopening.

- Global economy to expand 2.9% this year.

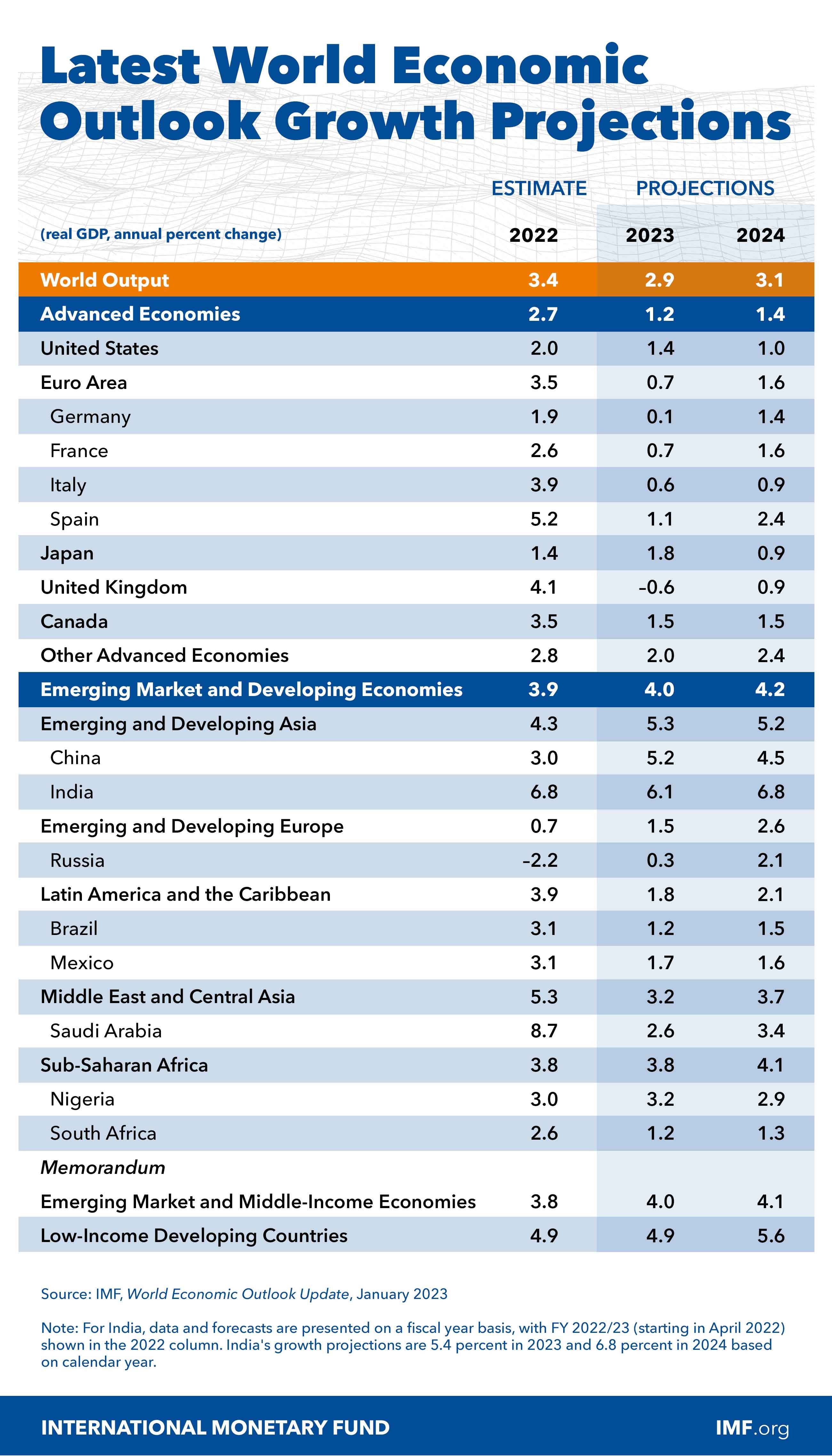

ISLAMABAD: The International Monetary Fund (IMF) has decreased the GDP growth rate projection for Pakistan from 3.5% to 2% for the fiscal year 2023.

According to IMF’s World Economic Outlook (WEO), issued on Tuesday, the country’s GDP growth rate would rebound in the next fiscal 2023-24 up to 4.4%.

The projection by the Washington-based lender, which is in talks with Pakistan regarding the revival of a loan programme stalled since months, is the same as predicted by the World Bank earlier this month.

In its report, titled “Global Economic Prospects” released on January 12, the WB predicted Pakistan's economic growth to reduce to half — down by 4% to 2% — for the current fiscal year, owing to the precarious economic situation and devastating floods.

Global outlook

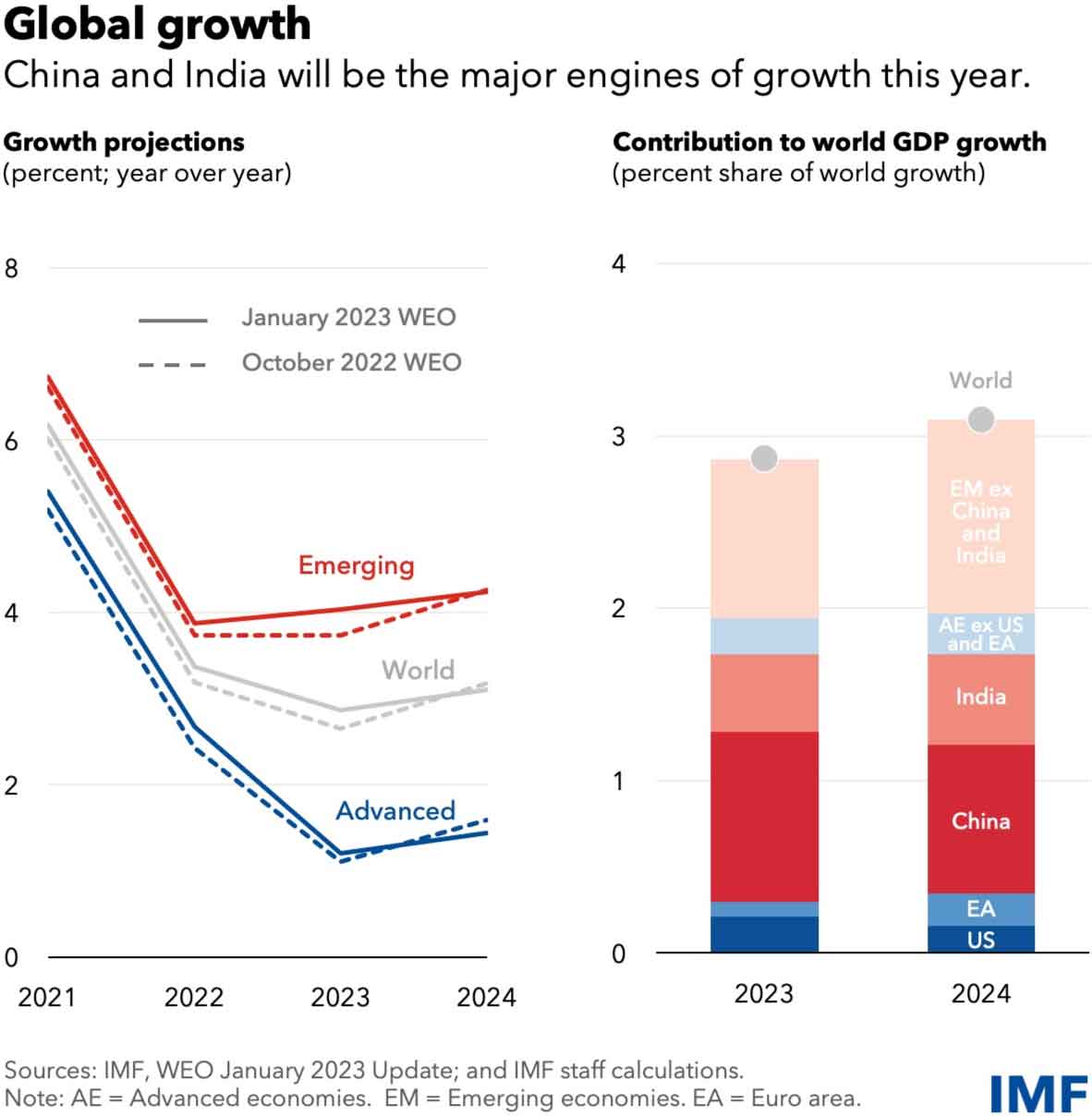

In its latest report, the IMF has raised the 2023 global growth outlook slightly due to "surprisingly resilient" demand in the United States and Europe, an easing of energy costs and the reopening of China's economy after Beijing abandoned its strict COVID-19 restrictions.

It said growth would still fall to 2.9% in 2023 from 3.4% in 2022, but its latest World Economic Outlook forecasts mark an improvement over an October prediction of 2.7% growth this year with warnings that the world could easily tip into recession.

For 2024, the IMF said global growth would accelerate slightly to 3.1%, but this is a tenth of a percentage point below the October forecast as the full impact of steeper central bank interest rate hikes slows demand.

IMF chief economist Pierre-Olivier Gourinchas said recession risks had subsided and central banks are making progress in controlling inflation, but more work was needed to curb prices and new disruptions could come from further escalation of the war in Ukraine and China's battle against COVID-19.

"We have to sort of be prepared to expect the unexpected, but it could well represent a turning point, with growth bottoming out and then inflation declining," Gourinchas told reporters of the 2023 outlook.

Strong demand

In its 2023 GDP forecasts, the IMF said it now expected US GDP growth of 1.4%, up from 1.0% predicted in October and following 2.0% growth in 2022. It cited stronger-than-expected consumption and investment in the third quarter of 2022, a robust labor market and strong consumer balance sheets.

It said the euro zone had made similar gains, with 2023 growth for the bloc now forecast at 0.7%, versus 0.5% in the October outlook, following 3.5% growth in 2022. The IMF said Europe had adapted to higher energy costs more quickly than expected, and an easing of energy prices had helped the region.

Britain was the only major advanced economy the IMF predicted to be in recession this year, with a 0.6% fall in GDP as households struggle with rising living costs, including for energy and mortgages.

China reopens

The IMF revised China's growth outlook sharply higher for 2023, to 5.2% from 4.4% in the October forecast after "zero-COVID" lockdown policies in 2022 slashed China's growth rate to 3.0% — a pace below the global average for the first time in more than 40 years. But the boost from renewed mobility for Chinese people will be short-lived.

The Fund added that China's growth will "fall to 4.5% in 2024 before settling at below 4% over the medium term amid declining business dynamism and slow progress on structural reforms."

At the same time, India's outlook remains robust, with unchanged forecasts for a dip in 2023 growth to 6.1% but a rebound to 6.8% in 2024, matching its 2022 performance.

Gourinchas said together, the two Asian powerhouse economies will supply over 50% of global growth in 2023.

He acknowledged that China's reopening would put some upward pressure on commodity prices, but "on balance, I think we view the reopening of China as a benefit to the global economy" as it will help ease production bottlenecks that have worsened inflation and by creating more demand from Chinese households.

Even with China's reopening, the IMF is predicting that oil prices will fall in both 2023 and 2024 due to lower global growth compared to 2022.

Risks, up and down

The IMF said there were both upside and downside risks to the outlook with built-up savings creating the possibility of sustained demand growth, particularly for tourism, and an easing of labor market pressures in some advanced economies helping to cool inflation, lessening the need for aggressive rate hikes.

But it enumerated more and larger downside risks, including more widespread COVID-19 outbreaks in China and a worsening of the country's real estate turmoil.

An escalation of the war in Ukraine could further spike energy and food prices, as would a cold winter next year as Europe struggles to refill gas storage and competes with China for liquefied natural gas supplies, the Fund said.

Although headline inflation has come down in many countries, a premature easing of financial conditions leaves markets vulnerable to sudden repricings if core inflation readings fail to come down.

Gourinchas said core inflation may have peaked in some countries such as the United States, but central banks need to stay vigilant and be more certain that inflation is on a downward path, particularly in countries where real interest rates remain low, such as in Europe.

"So we're just saying, look, bring monetary policy slightly above neutral at the very least and hold it there. And then assess what's going on with price dynamics and how the economy is responding, and there will be plenty of time to adjust course, so that we avoid having overtightening," Gourinchas said.

— With additional input from Reuters